In Gold We Trust, 2023: SHOWDOWN

From the Silver Stock Investor newsletter | June 2023

This content is made possible through subscriber support. Not a subscriber yet? Click here to see our subscription options or click the button below to subscribe to the full Silver Stock Investor letter.

The highly anticipated annual In Gold We Trust (IGWT) report for 2023 was recently released. Their silver section, Silver’s Time to Shine? does an excellent job of reviewing the silver market and potential.

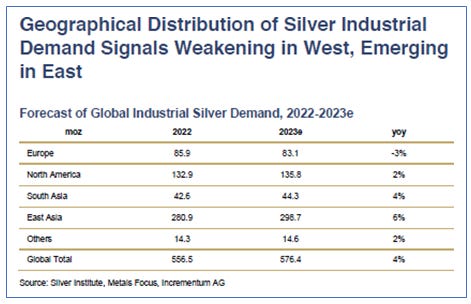

The report leverages the Silver Institute’s 2023 World Silver Survey, and expands on that with its own conclusions. A noteworthy point is how the industrial demand for silver is shifting from West to East.

Both South Asia (4%) and East Asia (6%) look to be where the bulk of industrial demand growth will from from. Again we focus on solar, because as the report points out, the Silver Institute’s survey says PV demand was up an astounding 28% last year. And IGWT produced an eye- popping chart which indicates silver demand will be 7 times the amount used in 2021. That’s because solar PV power generation will need to grow at a breakneck 25% year over year until 2030 to meet the IEA’s projections for net zero targets.

I believe that the Silver Institute’s projections for silver demand from solar PV for 2023 are too conservative at 15%. That would peg this year’s requirements at 161Moz. But given the previous chart, and this next two, you’ll see what I mean. This chart shows the different silver loadings per panel based on three different technologies. PERC uses 80 mg, TOPCON 100-120 mg, and HJT 200-220 mg.

The dominant technology right now is PERC. But the other two are considerably more efficient, in part because they use more silver. And according to Rystad Energy, a research consultancy, TOPCON and HJT are rapidly crowding out PERC. They recently pointed out that they expect this year nearly 80% of new solar cell manufacturing will use either TOPCON or HJT.

My esteemed colleague, Chen Lin, who is also uber-bullish silver, sees 2023 as “the year of TOPCON”. IGWT goes on to quote the University of New South Wales in Australia: “The transition to high-efficiency technologies including TOPCON and SHJ could greatly increase

silver demand, posing price and supply risks”. They point out that has motivated some, like the Fraunhofer Institute for Solar Energy Systems to find ways to reduce silver loadings. Still, TOPCON and HJT are expected to represent more than 50% of solar panels by 2025.

Switching gears to the automotive industry, IGWT highlights how hybrids and EVs require up to double the amount of silver that internal combustion engine vehicles need. And last year’s global sales of EVs at 10M units is expected to be far surpassed this year, reaching 14M units. Of course, this is in large part being driven by government policy. In the EU, for example, they are pressing forward with ensuring all new cars registered in 2035 are zero-emission. The US and UK have also moved aggressively on policy towards similar goals. And China, where 60% of global EV car sales, they’ve already surpasses their 2025 target for new EV sales.

At the same time IGWT quotes my own calculations to bring some sobriety to the EV silver demand outlook:

However, we must not overestimate the impact of EV demand on total silver demand. Peter Krauth’s calculations suggest EV demand could be as low as 1.0% of total silver demand, or 1.3% of total supply (including recycling), and 1.6% of total mined supply. These estimates are based on an average EV silver consumption of 1.29 troy ounces (40g), with total EV sales in 2022 of 10mn equating to an annual silver demand of 1.24bn ounces.

So, although silver demand from EVs is growing rather quickly, it’s starting from a very low level when compared to the clearly dominant solar sector.

The report delves into jewelry demand, where the story was all about India. I covered that in my May issue, so I won’t bore you with that again. Suffice it to say that with nearly 60% of world population, Asia dominates silver consumption through jewelry and investment demands, as well as the solar angle.

One especially effective chart is that of the silver market, in tonnes, 2013 – 2023e.

That red blob on the far right show just how dramatically the silver market swung in 2021 and 2022 to a huge deficit of 237Moz last year, wiping out more than the previous 11 years’ worth of surpluses.

They go on to put the silver industry’s size into perspective. At just $18 billion, it’s almost undetectable on the following chart, that pits it against the gold mining industry, the S&P Energy

Sector, the combined silver, gold, copper, precious metals and diversified mining industry, and finally Apple.

Even the gold mining industry, by itself, is a whopping 25 times the size of its little silver brother. Naturally that makes silver hypersensitive to large purchases, like when Warren Buffett bought silver in a big way in 1997. As the report cites Citi: “The silver market is absolutely tiny relative to the scale of speculative interest volatility, so investor buying often has an outsized impact on prices”.

Still, the high correlation between silver and gold of near 80% over the past two decades suggests that gold too remains a very big driver for silver, which tends to follow gold’s lead for direction, then outpace it.

The last main point, worth considering given the still relatively high risk of recession, is silver’s performance during such economic events.

As their proprietary Incrementum Recession Phases Model (IRPM) suggests, silver does well in the lead up to a recession, then loses an average of 9% during a recession, however with a lot of variability. They also point out that silver has performed well in the early and late phases of past recessions. And as I suspected, they show that silver does particularly well in the last (reflation) phase of recession, as economic recovery stokes industrial demand.

IGWT reaches a similar conclusion to mine. We have ideal conditions for silver to perform well for years, and maybe even decades to come. The green transition will drive industrial demand, spearheaded by solar, whose adoption of technological efficiencies will spur even higher consumption. But recession could weigh on the metal, at least temporarily, and is likely to be dependent on reaction by governments by way of stimulus program. What’s more, limited capital expenditure by silver miners suggests supply will struggle to grow even minimally. This will perpetuate the current deficit market balances for years forward.

As they put it, “in light of the factors discussed, the future of silver shines bright, arguably with a glow more radiant than previous bull markets.”

I could not have said that better myself.

To see our subscription options, please click here. To subscribe to the Silver Stock Investor now, please click the button below.